Betting on Cement | Eagle Materials $EXP Full Write Up

Why I'm long Eagle Materials stock ($EXP). Full deep dive on the cement business.

So often, investors focus on what changes in the world. Such and such may be the dominant technology today, but once XYZ happens, that could change. “Disruption” has become the new “.com” and investors are constantly on the watch for any and every new idea that will change the game. Will self-driving cars make Uber obsolete? Or will Uber’s network abilities position it as the winner of the self-driving revolution? Will Google lose its search business to LLM’s? Or will LLM’s make Google’s search business just that bit more powerful? What about Airbnb vs Hotels? Or renewables vs fossil fuels? So many questions, so much on the line, and so much money to be made in guessing correctly!

But me? I don’t like change. I hate thinking about change because it fundamentally requires making guesses about the future; something that seems easy in hindsight, but proves virtually impossible in practice. Change is often times unavoidable, but I find this to be a very frustrating starting place as an investor. I figure, the less “fortune telling” i’m forced to do, the better. Behind all (or at least most) of my investment ideas, lies some bigger and more broad idea that I can cling to. I need a foundation that is solid before I can construct a winning thesis on top of it.

So here is my big idea: cement is heavy.

Thats it. The basis of my bet on cement has to do with the very quality that makes it useful in the first place; its weight. You want to build a strong structure? You need cement. There’s no easy way around humanity’s need for cement, and - much like the structures it helps build - cement ain’t goin’ anywhere. Its all around you. And its the weight of that cement, and the “unit economics” created by that weight, that make up the foundation of my idea.

Bare with me here…I swear i’m going somewhere with this.

Remember Newton’s second law from physics class? F = MA?

That is: Force = Mass x Acceleration.

But now lets flip it: A = F/M (acceleration is equal to force divided by mass)

Think of “force” as the energy (and therefore money) needed to move a truck. Mass is the weight of what its carrying, and acceleration is the increase in speed needed to, you know, make it move! That means that as you increase mass (weight), you need more force (i.e energy and therefore money) to actually move that mass.

This is the long way of saying that you gotta pay big bucks to move heavy stuff. With raw materials like copper, coal, oil, ect, that isn’t a big issue. Those things can be sold at a high enough price/ton that the cost to ship it isn’t a deal breaker. Cement is another story though. You need a lot of this stuff to build a structure, and fortunately cement is proportionally cheap to produce per ton. Thats great - unless you have to ship that cement. The cost of shipping cement starts becoming a big problem the further you move it. The cost of fuel alone significantly restricts how far you can transport that cement before your margins turn negative. I will go into more detail later on this dynamic, but the principle is the important thing here. Reason being that, if cement producers can’t make money shipping it, then the buyers have to buy it locally. The result? A highly fragmented and localized cement market; one in which the lowest cost local producer becomes a natural monopoly. All of that information can actually be found in the annual report for the company I’m talking about today: Eagle Materials $EXP.

But first, lets talk about cement itself.

What is cement anyways? Well, basically its a key ingredient in the making of concrete. I’ve accidentally written the word “concrete” when I meant to say “cement” at least 10 times by now - thank god for cmd+f.

Think of it like this, cement is the flour and concrete is the cake itself. Fortunately for Eagle Material’s shareholders, there is no gluten free option for concrete. But back to cement!

You want to make some cement? Easy. Go get some limestone and clay (or shale) and grind it up. Then put it in a kiln and heat it to ~1,450 °C. Then you’ll have something called “clinker.” Mix that clinker with gypsum (a very common mineral), and presto! You have cement. Add some water and you'll get a very heavy goop that will eventually dry and harden into something akin to stone. When cement hardens it looks suspiciously like “Portland stone” from England, which is why the most common type of cement is called “Portland Cement.”

So if thats cement, then what is concrete?

Like I said, the cement is just the flour and concrete is the cake. So, if you want to make concrete, just take your cement and mix it with water, sand, and gravel (called “aggregates).” You mix the glue-like cement with what amounts to sand and rocks and you end up with another “stone-like” material called “concrete.” So if you’re driving down a concrete-highway you’re basically driving on rocks and gravel (aggregates) being held together by cement. Those giant trucks you see with the giant spinning mixer? Well thats concrete being mixed before it arrives on the job site - ready to pour.

So, while cement has a few uses besides being the sole binding agent in concrete, the vast majority (~97%) of cement is put to use in the making of concrete.

So what do we need all this concrete for? Well…

Concrete has a way of showing up almost everywhere you look in the building environment. It serves as the anchor for the foundations and floor slabs of houses, apartment towers, office blocks, hospitals, stadiums, schools, data-centers and warehouses, while also forming the tilt-up walls and precast columns that let those structures rise quickly. Moreover, concrete (and therefore cement) is the backbone of our transportation systems; think concrete highways, city streets, airport runways, bridge decks, piers, abutments, cable-stay pylons (whatever that is), railway ties, ballast-less track beds, and the heavy quay walls of our ports.

But what about the stuff you don’t see in your day today like civil-engineering mega-projects? Well they rely on it too! Imagine all the cement needed for gravity dams and spillways, flood-control levees, canal locks, storm-surge barriers, water and wastewater treatment plants, underground tunnels and subway linings, as well as the gigantic silos, containment berms, and the industrial floors of refineries. LNG terminals, petro-chemical complexes, and power stations all require vast amount of cement. Hey, speaking of power…cement also plays a role in the energy sector! Cement secures oil and gas well casings deep underground, forms the massive pads for wind turbines and transmission towers, and provides the heavy foundations for solar-tracker arrays. Roller-compacted and ultra-high-performance concretes derived from Portland cement make it possible to build rapid-placement dams, long-span bridge girders, blast-resistant panels, and thin architectural facades. And finally, closer to home, cement ends up in driveways, patios, sidewalks, curbs, retaining walls, swimming-pool shells, masonry mortar and grout, and in shotcrete sprayed onto basement walls, tunnel roofs, or steep slopes to keep the ground in place.

In short, if a structure must be rigid, durable, and able to handle compression or weather, Portland-cement made concrete is the sole material that makes it possible. Have I convinced you cement is important?

Ok ok, you’re thinking “I get it, cement is everywhere, but its also a commodity! One truckload of cement is basically as good as another.” And while i’m sure thats mostly true, my thesis doesn’t rely on one company having some special “cement patent” or anything. Moreover, Eagle Materials doesn’t have a fancy “brand that builders trust” either. Instead what they have is control of the supply chain in all the geographies they operate in. They have their own limestone, clay, and gypsum reserves that enable them to produce a finished product at a lower cost than their competition. This makes them the lowest cost producer wherever they operate.

I’m gonna say that again because its so important. Eagle Materials is the lowest cost producer of cement because there aren’t four other companies all taking a cut on production and delivery of the raw materials needed to make the cement. This is what people in nice suits call “vertical integration.” When you sell a somewhat fungible type commodity (i.e cement), its tricky to really compete on anything besides price. This means that wherever Eagle operates, its a powerful little monopoly.

Now, usually U.S producers are not the “lowest cost producer” of anything. Somewhere in the world there always seems to be someone else making something cheaper - which really is the most important quality of a truly fungible commodity. But as I mentioned at the beginning, there is a basic law of physics which restricts people in far away places from transporting cement to Dallas or Oklahoma and making a profit on it. This discrepancy between weight and “cost to transport” forces concrete (and therefore cement) to remain a highly localized and fragmented business. When I said “far away places” earlier, I really just meant 150 miles away or less; thats 50 miles shorter than the distance between NYC and Boston. After that you’re losing money on your concrete. Crazy right?

In their 2024 annual report, Eagle’s management puts it like this:

“Because of cement’s low value-to-weight ratio, the relative cost of transporting cement on land is high and limits the geographic area in which each company can profitably market its products. The low value to-weight ratio generally limits shipments by truck to a 150-mile radius from each plant, up to 300 miles by rail, and further by barge. Consequently, the U.S. cement industry is made up of regional markets rather than a single national selling market.”

Now imagine trying to transport your product even just 75 miles, and when you show up Eagle Materials is still outbidding you because they’ve already spent two decades refining their operations; buying up limestone mines that make your already-thin margins look even thinner. Better to avoid the competition than take on losses. But hey, if you want to run your business into the ground thats fine with Eagle. They’ll wait patiently until the building cycle in your region hits a gully and just buy you out - at a steep discount I should add.

See, Eagle doesn’t just operate in one place. If business gets tough in Missouri, they can use profits from their Gulf Coast operations to make opportunistic acquisitions in Missouri. You may already be thinking that the cement business must be pretty capital intensive, and while that is very much true, Eagle’s high ROE tells a story of a company that deploys its capital very efficiently over time. The capital intensity of the cement business ends up serving as yet another moat; protecting Eagles dominant position. We’ll get into financial metrics a little later, but first…

Lets quickly back up and break down Eagles business segments from 2024:

Heavy Materials (Cement, Concrete, and Aggregates) = 60%

Cement = 52%

Concrete and Aggregates = 10%

Light Materials = 40%

Gypsum Wallboard (Drywall) = 33%

Recycled Paperboard = 5%

As you can see, cement and wallboard make up a collective 85% of the business (which is why I’m not spending much time on paperboard). That said, when it comes to concrete and aggregates, Eagle is happy to make acquisitions and grow this segment -so long as the price is right. Since cement is the key ingredient in concrete, you can imagine the cost advantages of combining the output of a cement plant with that of an aggregates quarry or pit mine.

Moreover, the value-to-weight ratio principal applies to all of their business segments; besides maybe that of the small paperboard business. Wallboard may have a bit of a larger “profitable radius” (~300 miles), but the fundamental idea remains intact. Ultimately, its this “physics-restricted unit economics” that enables Eagle to stay patient with their acquisitions and compete only with the more fragmented/less efficient local producers. While its true that - just like their competition - Eagle can’t move its product across the country from one plant to another, they can move their capital wherever they like. On top of that, Eagle Materials is able to invest in:

“state-of-the-art technology that lifts throughput, trims energy, and lowers carbon.”

Everything from better equipment to dispatch GPS systems helps Eagle meet the growing needs of their customers, satisfy emission standards of regulators, and reduce waste; thereby improving improving their margins and core-business strength. One might think higher emissions standards would hurt Eagles business, but it basically does the opposite. Eagle can afford to make these upgrades responsibly while many local producers simply cant. In many ways, when things get difficult for the cement business in the short term, Eagle actually benefits in the long run. Management talks about doubling earnings from peak to peak (a goal they’ve accomplished repeatedly). They can do this because they have the scale, balance sheet, and geographic diversification that regional competitors lack.

I always think about the wolf and the three little piggies; two of which have houses made of sticks. But then theres that third piggy, the one with the house made of stone (most likely held together by cement). Thats Eagle Materials.

Of course no one wants a wolf to come around and start destroying property value, but if the third little piggy was a true capitalist, he would see the opportunity to acquire the land of the other two piggies at a steep discount.

Now, I’m not sure if pigs engage in share buybacks, but Eagle does. Whenever the stock gets cheap or management has extra capital lying around they either buy up their competitors assets or they buy back shares. Its “rare” that the entire U.S materials segment suffers all at once, so Eagle usually has plenty of cash coming in the door from other operations to take advantage of any weakness in a specific regional market. They can then use their capital, scale, and expertise to re-vamp the beaten down asset.

Lets talk about geography for a minute.

Eagle Materials conveniently focuses on those regions that are growing faster than the rest of the country. I can probably let management explain this one:

“Demand for our products depends on construction activity, which tends to correlate with population growth. While the Company’s markets include most of the United States, except the Northeast, approximately 65% of our total revenue is generated in ten states: Colorado, Illinois, Kansas, Kentucky, Missouri, Nebraska, Nevada, Ohio, Oklahoma, and Texas. Population growth is a major driver of construction products and building materials demand. The population in these ten states is expected to increase approximately 11% between the 2020 census and 2050, compared with 7% for the United States as a whole, according to the latest update in February 2024 by Moody’s Analytics.”

I think its funny that despite being on completely opposite sides of the political isle, both Biden and Trump seem to need more of one thing: cement. Biden’s large scale infrastructure spending bills and Trump’s push for U.S Re-industrialization both require a ton of cement. The tailwinds of such policies are long lasting and create new tailwinds of their own. Of course, if you want to build a factory you need cement, but there always more to it than that. You also need a parking lot, roads to the factory, infrastructure to power the factory, drainage around the factory, housing for all the people working at the factory, and of course all of those new houses will need sheetrock in the walls and concrete in the driveways. I guess the point i’m trying to make is that development begets more development. And development always requires cement.

Moving on…

Gypsum Wallboard: what is it, and what is it good for?

I feel obliged to explain a bit about the other major segment of Eagle Material’s business - that is, the Gypsum Wallboard segment (33% of FY 24’ revenue). You may not have heard of gypsum wallboard before, but you probably know about “drywall” or “sheetrock.” All three of those are different names for the same thing. If you punch your wall right now there is a 97% chance that the material you break your hand on will be sheetrock/drywall/gypsum wall board - remember that they’re all the same thing. I say “97%” because there is also a 3% chance you hit “plaster board” which is different and also inferior material we no longer really use to build homes. I should clarify that these percentages actually refer to “new constructions” and not old ones. Back in the day plasterboard was more prevalent, but by now basically all new construction involves walls made exclusively from dry-wall (sheetrock/gypsum wallboard).

Remember gypsum? Its one of those key ingredients you need to make cement. So perhaps you’re already thinking how convenient it is that Eagle Materials needs gypsum for both of its largest business segments. Fortunately for you, I don’t really need to explain much about wallboard that you don’t already know about cement. The same principals apply here as did to the cement business; value-weight ratio, fragmented market, vertical integration, and irreplaceability.

Eagle owns and operates 5 different wallboard plants, and 4 of those 5 are supplied with Gypsum from Eagles own quarries. Much like the limestone mines supplying their cement plants, the gypsum quarries for Eagle’s sheetrock business allow them to compete on the ever important metric of price. Yet again, Eagle finds themselves as the lowest cost producer in their regional market.

While there are seemingly infinite uses for cement, sheetrock is really only good for two things; walls and ceilings. As a result, Eagle’s gypsum wallboard segment sees its demand coming from four markets: residential construction, repair and remodel, non-residential construction, and manufactured housing. As you would imagine, these markets ebb and flow with population growth, economic development, and the housing market in general.

Ok, to the numbers.

Now that you understand the game and the playing field, lets look at the scoreboard for a moment. Its one thing to have a qualitative understanding of a businesses advantages, but they still need to translate into healthy financial figures. Fortunately, this is very much the case for Eagle Materials. The story told by the companies financial statements is one of solid revenue growth, expanding margins, a healthy balance sheet, high returns on equity, and a consequential 14% annualized EPS growth rate over 10 years. They pay a very modest (0.5% ) dividend as well, but I choose to ignore that. I’m also not going to talk about EBITDA because its insane to look at a capital intensive business like cement without accounting for depreciation (or interest for that matter).

Ok lets break it down. Starting with the top line.

Over a 10 year period EXP’s CAGR for revenue was 7.8%, and over 5 years it was 10%. Below is a chart showing their revenue going back 15 years to 2010:

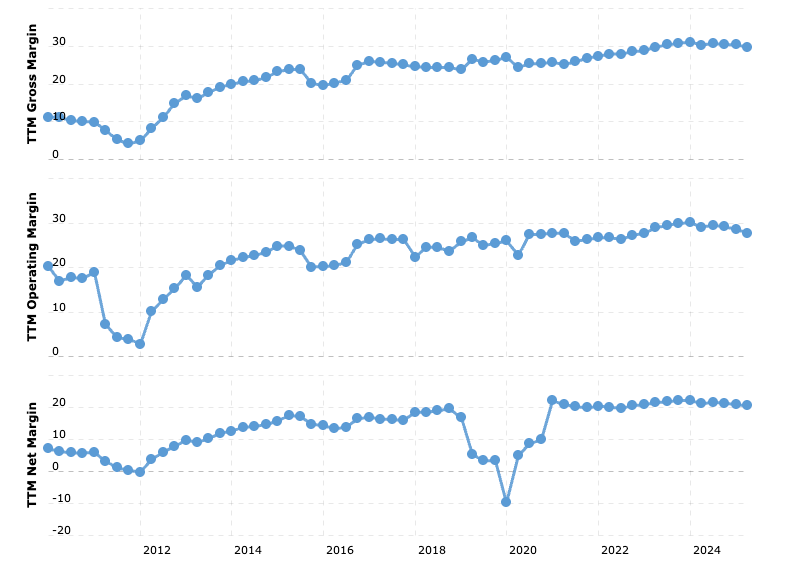

Now lets take a look at margins. According to google, the industry average gross margin for cement is 5-10%. For Eagle Materials it is a whopping 30%. And if you think that 30% gross margin gets eaten away by operating costs, taxes, or interest, you are sorely mistaken. Eagles net profit margin has grown to a fairly juicy and stable 20%. For any business, a 20% margin is great, but for a cement company thats really good:

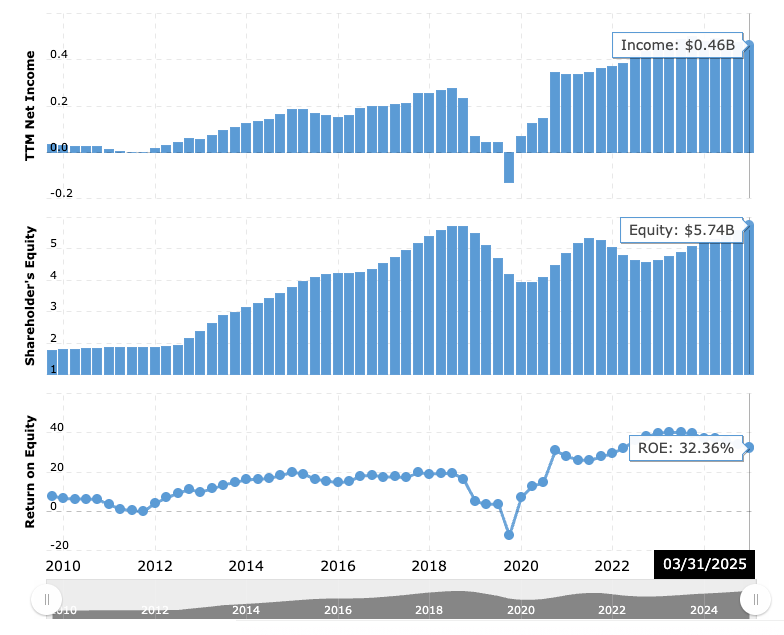

If you didn’t believe in my “opportunistic little piggy” story, take a look at Eagles ROE. For a business that is fundamentally capital intensive, this chart depicts true capital allocation discipline on the part of management:

32% ROE is excellent considering debt is only 2x net-income. This means that, despite acquisitions and cap-ex, Eagle gets a marvelous return on the capital they deploy.

And what about buybacks? Well here is yet another chart showing EXP’s shares outstanding declining 34% over 10 years from 50 million in 2015 to 33 million today:

Moreover, the balance sheet is healthy with net-debt = less than 2 years of net-income (my sweet spot). And all of this gets you a 10-year annualized EPS growth rate of 14%.

So what about price?

Today you can buy EXP for 15.6x their TTM earnings and 13.7x forward earnings. Lets forget the forward figures for a minute. As of today with a share price of $215, Eagle Materials sells for a pre-tax earnings yeild of 8%. That means that assuming no growth in the business, you get 8% on your money - not amazing, but not a premium either. Below is a chart of EXP’s historical TTM PE ratio:

Historically it does look a little bit cheap? Although probably 15.6x earnings is only average over the last 5 years. Maybe not a screaming bargain relative to history, but certainly a great value for what I get. Ultimately, I absolutely expect earnings to continue to grow at their historical average - if not faster. But its nice to know i’m not paying up for that growth like I would in the tech sector. Its also nice to know some new AI startup wont come out the darkness and eat the business. Even if Tesla’s Optimus robots end up working construction they’ll still be building with cement.

Parting Thoughts

While cement may be one of the most mundane businesses on Earth, the way Eagle operates within the segment is remarkable. Its margins trounce the averages and its ROE looks better than plenty of other, more “high-tech” businesses. These wonderful returns aren’t a fluke either. They’re a result of structural unit economics within cement industry; a battlefield in which Eagle has the high ground - and knows it too.

No one looks at concrete and imagines high returns, so the business is perpetually undervalued. That would be a bad thing if management didn’t happily buy back its shares at that cheaper price. Without any real competition on the horizon, Eagle can focus on opportunistic acquisitions that firm up their position as a regional monopoly, and expand their reach into new markets. Moreover, bad news is good news for these guys. Whenever we enter the next recession, i’ll be able to sit back comfortably; knowing that Eagle is probably making better investments than they were before. 14% EPS growth per year may not seem groundbreaking, but for me that is a wonderful return considering how confident I am in actually receiving it. Eagle is a company I own a lot of, and its one I plan to hold for the long term. It has a long runway of growth ahead of it and I love the business, the management, the numbers, and the valuation. All of that earns it a place as a core position in my portfolio.

A lot can change in this world, but the material foundation of our civilization is fixed, cast in stone, and held together by cement.

Credit where credit is due.

I didn’t find Eagle Materials by accident. I heard about it from the

substack which I highly recomend. While those guys didn’t end up buying it, their write up was enough to make me curious. After some research and pontification I started buying Eagle in early 2025 and added to the position during the tarrif sell-off. I also recently added more after Eagle missed analyst expectation on the last quarter and the price dipped a little. Regarding earnings expectations by the way, its important to note that only 3 analysts are actually making those projections for Eagle. So beware the forward looking metrics in this case in particular.Talk to ya later

-Peter

Really great post !

This was a brilliant breakdown—turning something as mundane as cement into a compelling investment thesis takes real insight. The physics lens (F = MA) to explain localized monopolies is especially sharp.